AYTA Exclusive

Analysing page-by-page the Legal Technology Software Market Report by Alkali Partners (an M&A and capital‑raising bank for tech) published in November 2025. (“Alkali Report”). The report highlights the deal data through Q3, 2025, and includes an estimate of 19 deals for Q4 2025 till November.

Author :

AYTA LegalTech Consulting

Published :

January 7, 2026

.png)

Analysing page-by-page the Legal Technology Software Market Report by Alkali Partners (an M&A and capital‑raising bank for tech) published in November 2025. (“Alkali Report”).

You can think of the Alkali Report as a narrative about “what’s going on in legaltech money in 2025” rather than a finance document: where capital is flowing, what worries investors, and what gives them confidence. Below is a page‑by‑page style explanation in plain language, with references to similar 2025 legaltech reports so you can connect the dots.

The report highlights the deal data through Q3, 2025, and includes an estimate of 19 deals for Q4 2025 till November.

Imagine discussing this report with your colleagues to explain where the money is flowing in our industry right now in the legaltech and where your business stand presently.

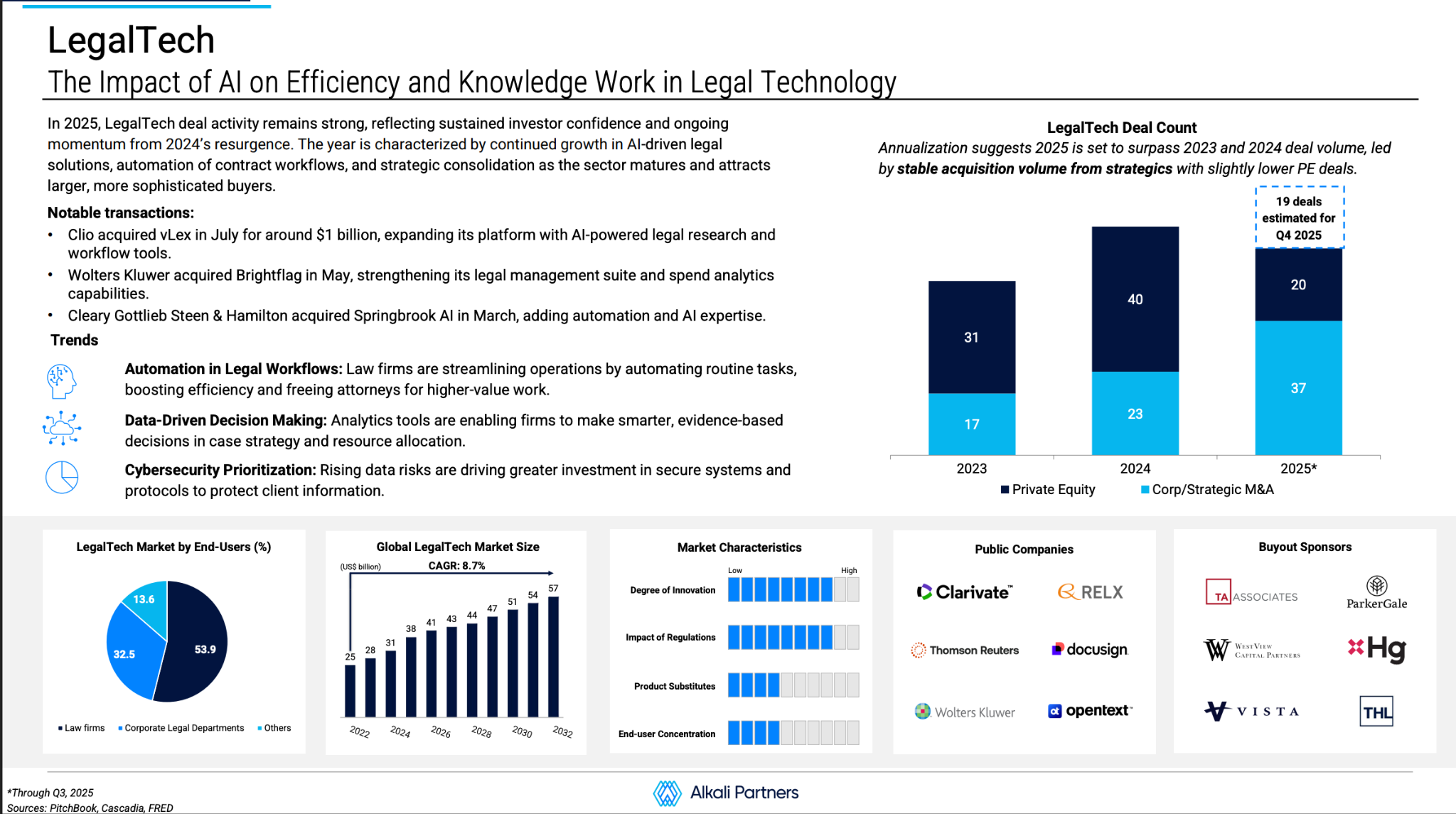

Page 1 is about the "Hook." It explains the state of investment in legaltech since 2020.

2020–2021 was the “party” (easy money, high valuations); 2022–2023 was the “hangover” (funding slowdown, valuation cuts); and 2024–2025 is the “sorting phase” where serious products and stronger companies survive and weaker ones get bought or die.

The report highlights how after a quiet period in 2023 and 2024, the checkbooks are opening again. The "impact" they are highlighting is that AI has forced a reset. Investors aren’t just looking for "safe" bets anymore; they are aggressively funding companies that can prove they are automating legal work, not just digitizing paper.

The Takeaway for You: The market has shifted from "growth at all costs" to "efficient growth." If you are pitching to investors in 2025, they don't just want to see user numbers; they want to see how your software becomes essential infrastructure for a law firm.

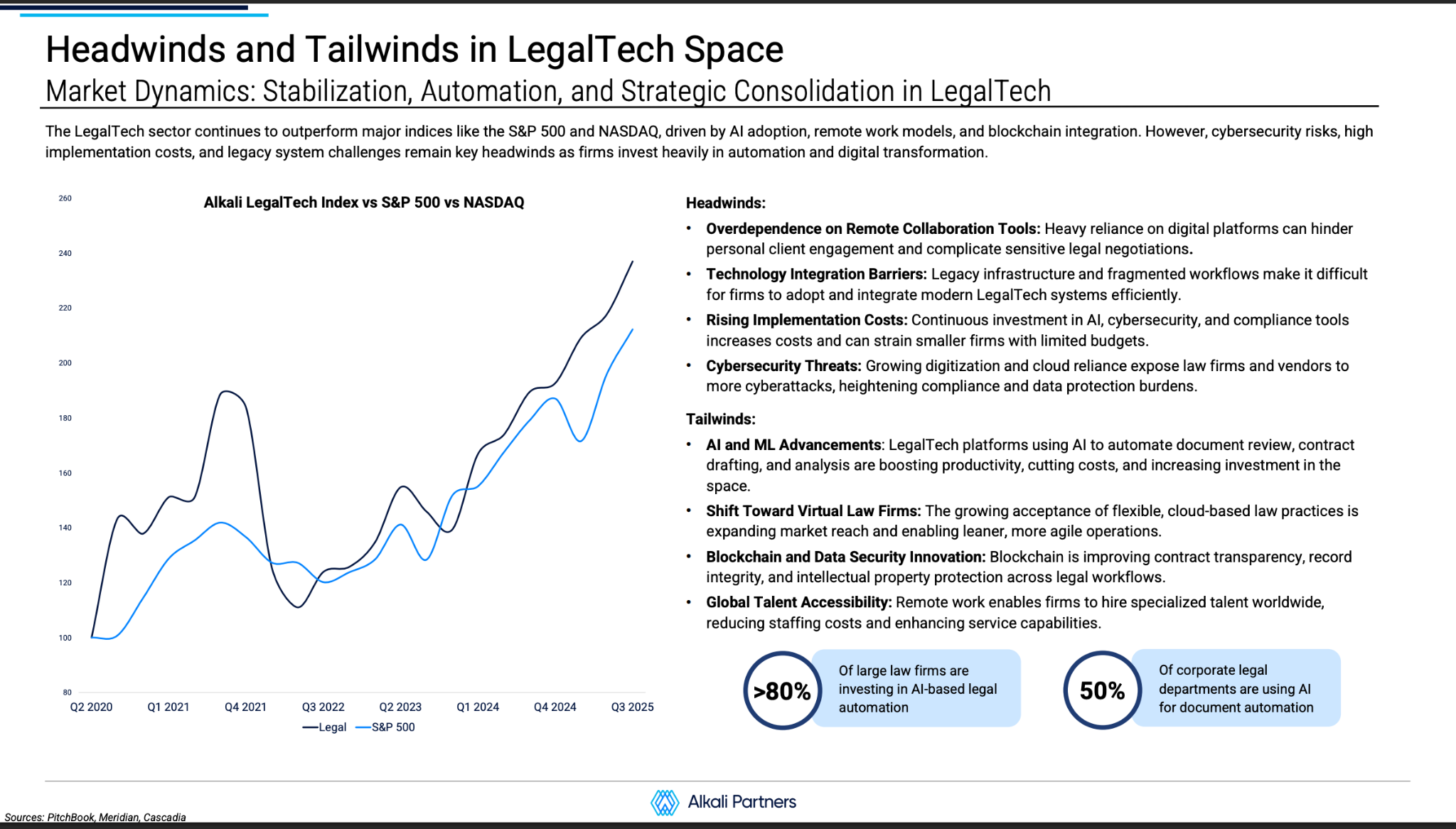

Founders often skip this, but it’s crucial to understand this section which explains the external forces pushing you forward or holding you back.

As per the report, typical 2025 headwinds are Higher interest rates / cost of capital; Valuation reset and Slower VC deployment & exits.

Highlighting the ‘Higher interest rates / cost of capital’, it emphasizes that money isn’t free anymore, so investors do fewer, more careful deals. Push harder on profitability, not just growth. Explaining the Valuation reset, it mentions that crazy 2021 multiples are gone; many SaaS and legaltech companies saw valuation cuts in 2023–2024. This means new rounds often get priced more conservatively. And buyers expect to pay “reasonable” multiples tied to revenue quality, retention, and margins. Further ‘Slower VC deployment & exits’, means that IPO and big exit markets were weak in 2023–2024, so some investors are cautious about pouring more money in without clear exit paths.

Tailwinds means the good news. Tailwinds are why legaltech is still attractive despite the headwinds. It highlights Structural demand for efficiency, AI & automation in legal workflows, and Consolidation opportunity gave boost to legaltech.

Corporate legal spend keeps growing, but GCs are under pressure to do more with less, that drives demand for matter management, spend analytics, CLM, and automation hence rise in the structural demand for efficiency.

Generative AI, contract review, eDiscovery automation, and AI‑powered research were the mainstream themes in 2025 as per Henchman’s “LegalTech Trends 2025 report. Investors liked products with clear AI‑driven productivity stories: “X% faster review”, “Y% fewer outside counsel hours”, highlighting the importance of AI & automation in legal workflows.

As per the report, there are too many point solutions; buyers (law firms, in‑house) feel tool fatigue. This sets up the stage for Consolidation opportunity, rollingup the plays for bigger platforms acquiring niche tools. Strategic buyers like legal publishers, practice management vendors filled product gaps through M&A rather than building everything.

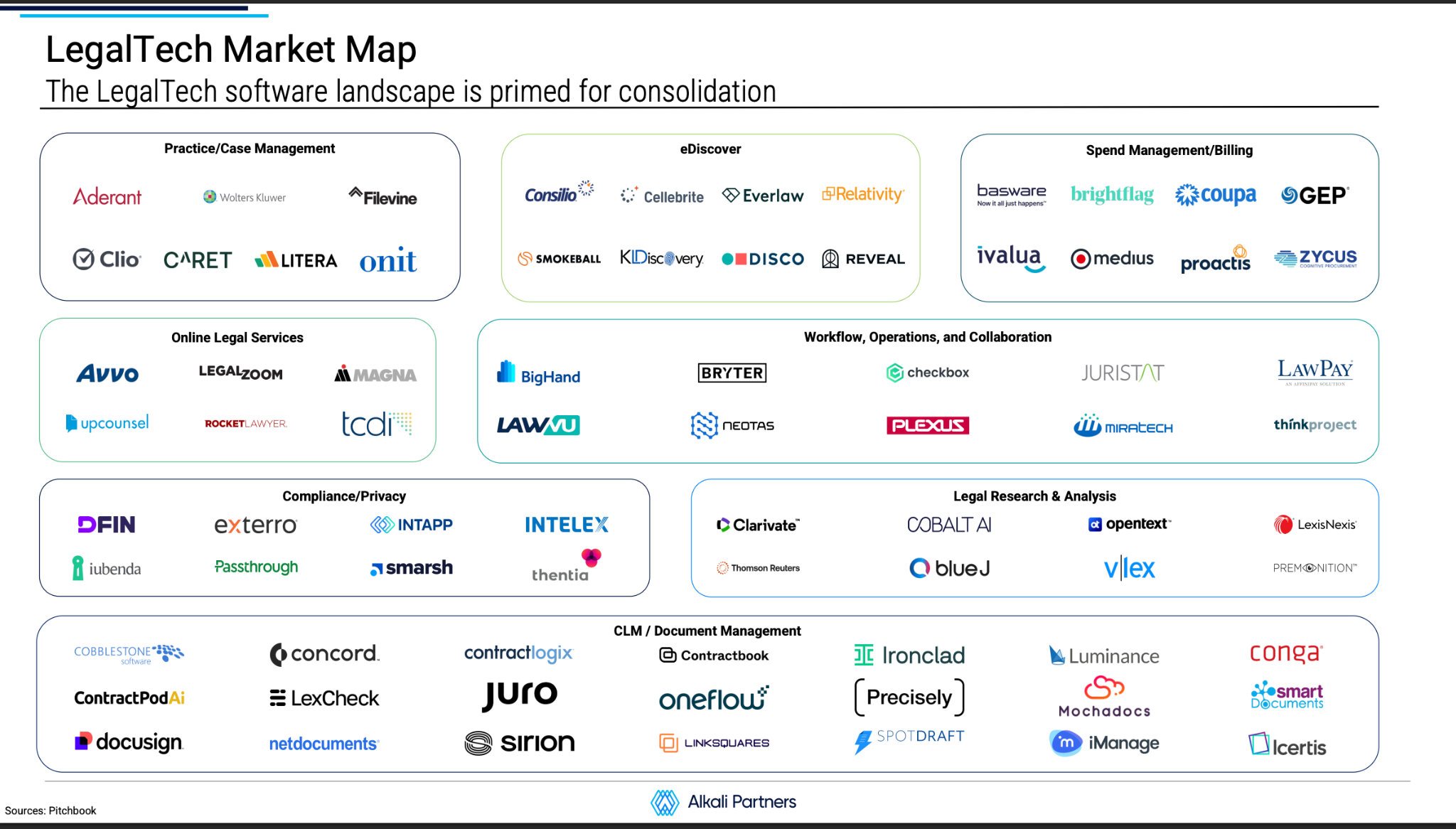

This page highlights what kinds of legaltech exist, and where does consolidation likely to happen?” The report clusters products into buckets like:

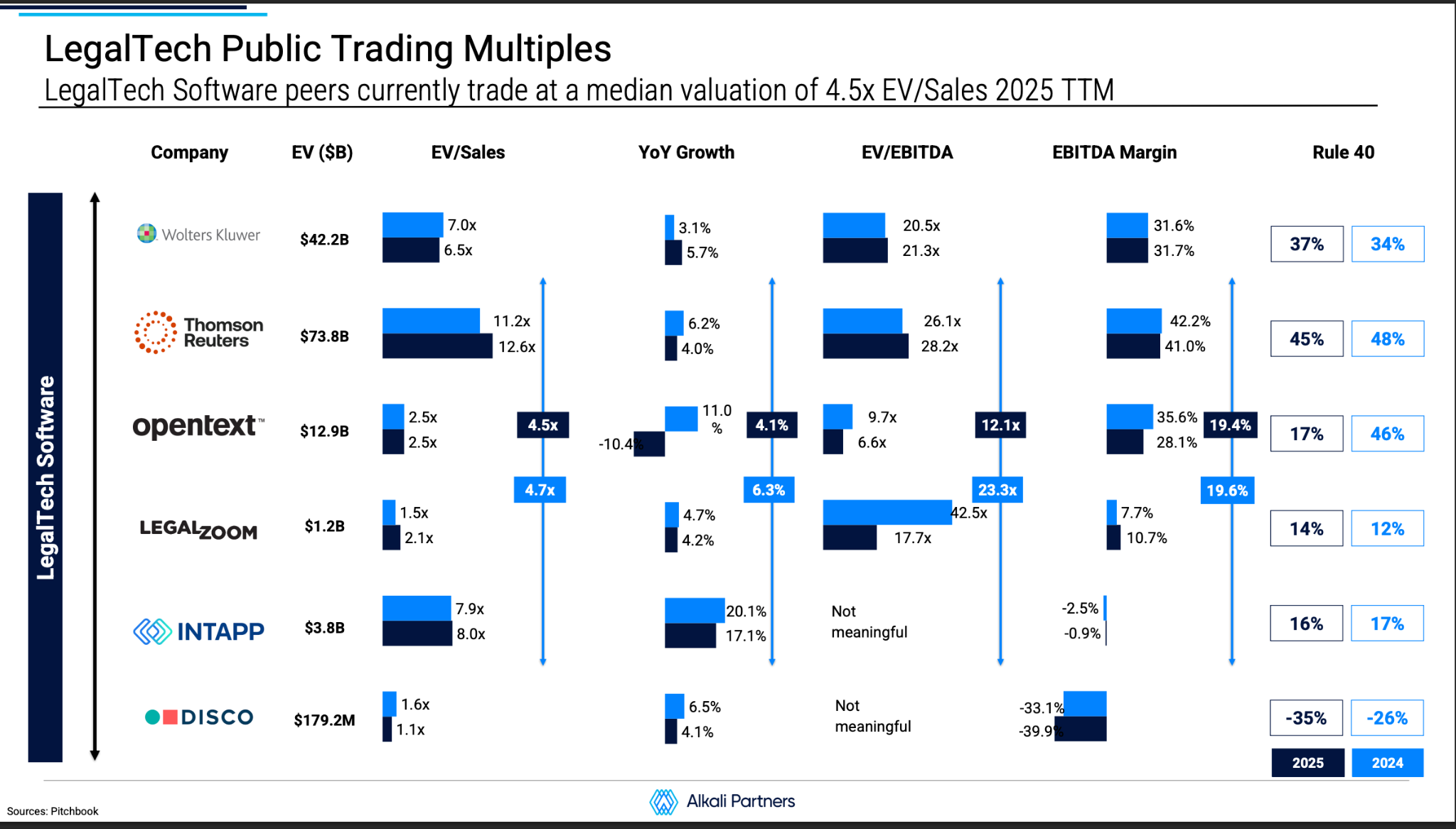

"I don't understand the finance side of things... what is this about?" - many of us as lawyers may have this question, but we all know that this is the most important section to understand the dynamics of valuation.

Yes, this is the most “finance‑ish” page, but conceptually it’s simple: Let me explain.

The Alkali Report highlights something like “publicly traded legaltech/ software peers currently trade at a median valuation of X× revenue (or Y× EBITDA).” The chart typically splits into:

Simplifying it more:

These public multiples create a “ceiling” and “reference point” for private deals. If public legaltech companies are at, say, 5–7× revenue, it becomes hard to justify 15× in a private round unless your growth/margins are exceptional.

They also inform M&A pricing. Strategic buyers usually won’t pay much more than what their own stock is valued at, adjusted for:

When they say "peers currently trade in the median valuation," they are giving you a benchmark.

Example: If the median multiple is 6.0x, and your startup makes $2 Million in revenue, a rough valuation might be $12 Million (2m x 6).

Why this matters: In 2021, these multiples were crazy (like 20x or 50x). In 2025, they have likely "stabilized" back to normal levels (around 5x–8x for good companies).

Notes from Meridian and broader SaaS commentary in 2025 indicate that multiples bounced from 2023 lows but remain below 2021 peaks, settling into a more “rational” band.

Think of this slide as the report giving investors and founders a benchmark: “Here is the current ‘price per rupee of revenue’ that the public market pays for legaltech‑adjacent software in 2025.”

PS: Don't let an investor tell you your company is worth nothing. Highlighting the points elaborated here, you can say, "Public companies trade at [X] times revenue, so my high-growth startup should command a premium."

The Alkali Partners LegalTech Research Report dated November 2025 is a near‑full‑year snapshot of the legaltech investment landscape up to that point, not a complete four‑quarter 2025 dataset. It pulls together data from sources like PitchBook and other market trackers to describe how legaltech funding, valuations, and M&A have evolved through roughly Q1–Q3 and early Q4 2025, highlighting both headwinds such as higher capital costs and valuation resets, and tailwinds like structural demand for efficiency and AI‑driven tools. Like other November 2025 sector and legaltech reports, it should be read as “2025 year‑to‑date”: directionally accurate for trends and category dynamics, but not incorporating every deal and valuation move from the final weeks of the year.

Summarizing the report, it can be concluded that the market has stabilized. The 'free money' era is over, but the 'smart money' era is here. Investors are paying healthy prices (multiples) for software that solves real problems, particularly using automation. We are facing headwinds from client fatigue, but massive tailwinds from the industry's need to adopt AI.

In 2026: Your goal shouldn’t be just to grow; but to position yourselves on the 'Market Map' as a prime target for the consolidation happening right now."

Download the full the Legal Technology Software Market Report by Alkali Partners here.

Thanks & regards

AYTA LegalTechConsultingGet in touch at

reach@ayta-legaltech.comStay ahead and subscribe for expert legal tech updates, worldwide.