The article analyzes how global legaltech fundraising surged to about $4.3B in 2025, concentrating capital into a few AI-first platforms like Harvey, Clio, and Filevine while mid-tier point solutions faced consolidation or distress. It explains quarter-by-quarter deal patterns, profiles the major startups and investors, and outlines why 2026 is likely to bring platform dominance, sovereign legal AI, and the first large legaltech IPOs.

Oops! Something went wrong while submitting the form.

2025 was not just a “big” year for legal tech—it was the year the market chose its platforms and started ruthlessly consolidating everything else around them. With roughly $4.3 billion in estimated global fundraising, legal technology moved from AI experimentation to a full-blown platform and infrastructure play, led by a handful of aggressive category-defining companies like Harvey, Clio, and Filevine.

From AI experiments to platform wars

If 2024 was about pilots and proofs of concept, 2025 was about investors and customers backing a small set of platforms that can actually run legal work at scale, not just “assist” it. The narrative was dominated by Agentic AI—systems that draft, reason, and execute workflows with minimal human intervention—and by the emergence of the first plausible LegalTech decacorn candidates.

Two structural shifts defined the year:

Capital concentration: Mega-rounds went into a few vertically focused, AI-native platforms, while mid-tier point solutions were squeezed into M&A, pivots, or distress situations.

Ecosystem maturity: Most serious Series A+ companies are now 4–5 years old, indicating a shift from experimental tools to durable infrastructure with real usage and retention expectations from buyers.

Quarter-by-quarter: how the money moved

2025 followed a crescendo pattern: infrastructure and category bets in Q1, platform-scale bets in Q2, an explosion of unicorn and decacorn narratives in Q3, and a combination of mega-rounds and public distress signals in Q4.

Q1: The AI infrastructure war

The first quarter (January–March) was about establishing who would own the “foundation” layer of legal AI. Roughly $550 million was deployed, heavily skewed toward a few players building core models and workflows for sophisticated legal environments.

Harvey’s Series D: Harvey kicked off the year with a $300 million Series D led by Sequoia Capital and the OpenAI Startup Fund, reportedly around a multibillion-dollar valuation, signaling that generalist VCs now see vertical legal AI as a durable category rather than a niche.

Eve’s Series A: Eve, focused on plaintiff-side AI support, raised $47 million in an a16z-led Series A, positioning itself early in the “AI for plaintiff firms” niche.

The subtext: infrastructure is no longer just LLM access—it is secure workflows, data handling, integrations, and outcomes that match bar-level expectations, which is why capital concentrated in a small set of technically and commercially credible teams.

Q2: Global expansion and M&A staging

In Q2 (April–June), the tone shifted from “who can build” to “who can scale globally and consolidate adjacent workflows.” Total fundraising volume for the quarter is estimated at around $850 million, with two clear themes: global expansion and strategic M&A preparation.

Harvey’s Series E: Harvey pulled off a rare second mega-round in a single year, raising another $300 million led by Kleiner Perkins and GV, pushing its valuation toward the decacorn trajectory and funding aggressive global expansion across major law and corporate markets.

LegalOn’s US push: Japan-headquartered LegalOn expanded its footprint in the US contract review market with a $50 million Series C, underlining the global nature of AI contract review competition.

Clio–vLex: Clio announced a definitive agreement to acquire vLex for about $1 billion, marrying practice management with global legal research and intelligence and making its intent clear—to be not just the operating system of law firms, but also the primary gateway to legal knowledge.

Q2 made one thing obvious to global legaltech: scale now requires three pillars—workflow ownership, content/intelligence ownership, and AI orchestration across both.

Q3: Unicorns and vertical AI scale

By Q3 (July–September), the market had enough data to decide which platforms were “working,” and capital followed suit. Total volume rose to roughly $1.4 billion, driven by practice management giants and highly specialized vertical AI plays.

Filevine’s $400M Series E: Filevine, positioned as a legal operating intelligence system, raised $400 million in equity financing led by Insight Partners, with participation from Accel and others, solidifying its role as the operational backbone for litigation-heavy organizations.

Blue J’s Series D: Blue J’s $122 million Series D round, led by Oak HC/FT and Sapphire, doubled down on AI-based tax prediction—showing that niche but high-value domains like tax are now strong enough to support late-stage capital.

Eudia’s Series A: Eudia raised $105 million in a General Catalyst–led Series A to build intelligence for Fortune 500 in-house teams, indicating that corporate legal is now a first-class AI buyer, not just an afterthought.

Q3 also widened the platform narrative: it is not only about law firms anymore, but also about in-house departments and specialist practices that require deep domain and workflow alignment.

Q4: Mega-closers and the middle-market squeeze

Q4 (October–December) was both the most exuberant and the most unforgiving quarter, with roughly $1.5 billion in funding and highly public distress for some mid-tier players.

Clio’s landmark Series G: Clio closed a $500 million Series G led by NEA, reportedly at a $5 billion valuation, coinciding with the completion of the vLex acquisition and cementing Clio as a core operating system plus research platform for small and mid-market firms globally.

Harvey’s third raise: Harvey added another $160 million in late-year financing led by a16z, bringing its 2025 total to around $760 million and pushing its valuation to about $8 billion, making it the clearest decacorn candidate in legal AI.

EvenUp’s scale round: EvenUp raised around $150 million in a Bessemer-led Series E at a valuation north of $2 billion, validating the “AI for personal injury claims” category as a durable vertical.

Robin AI’s distress: In sharp contrast, UK-based Robin AI was marketed for a distressed sale after failing to secure a targeted $50 million funding round and facing mounting losses, despite earlier growth and recognition.

The message to global founders and investors: there is little appetite left for mid-tier, semi-differentiated tools—capital either wants category-defining platforms or sharply verticalized, high-ROI products.

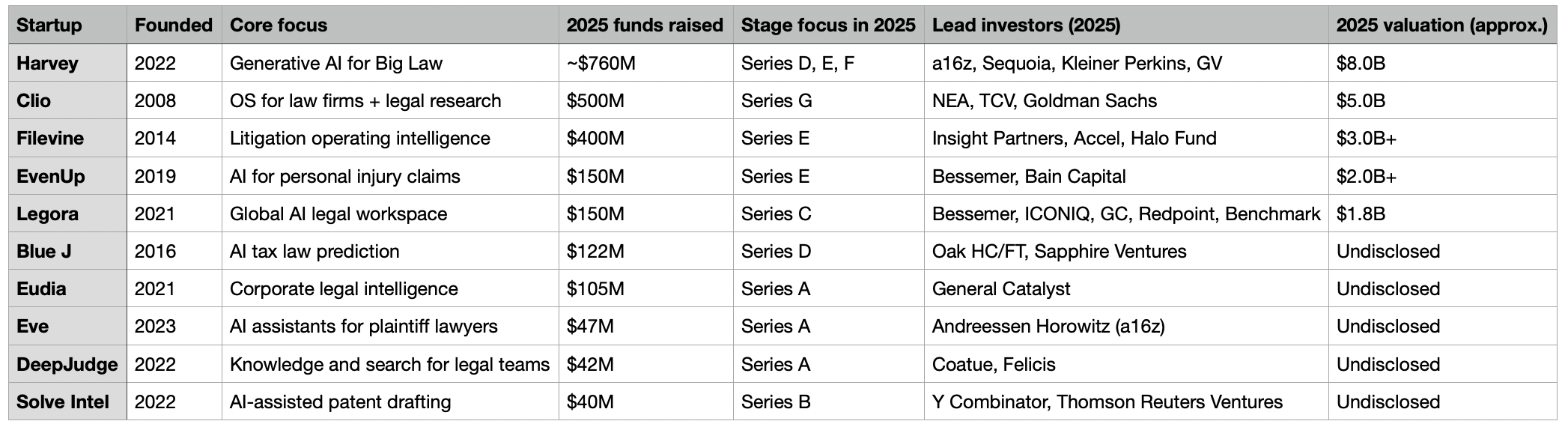

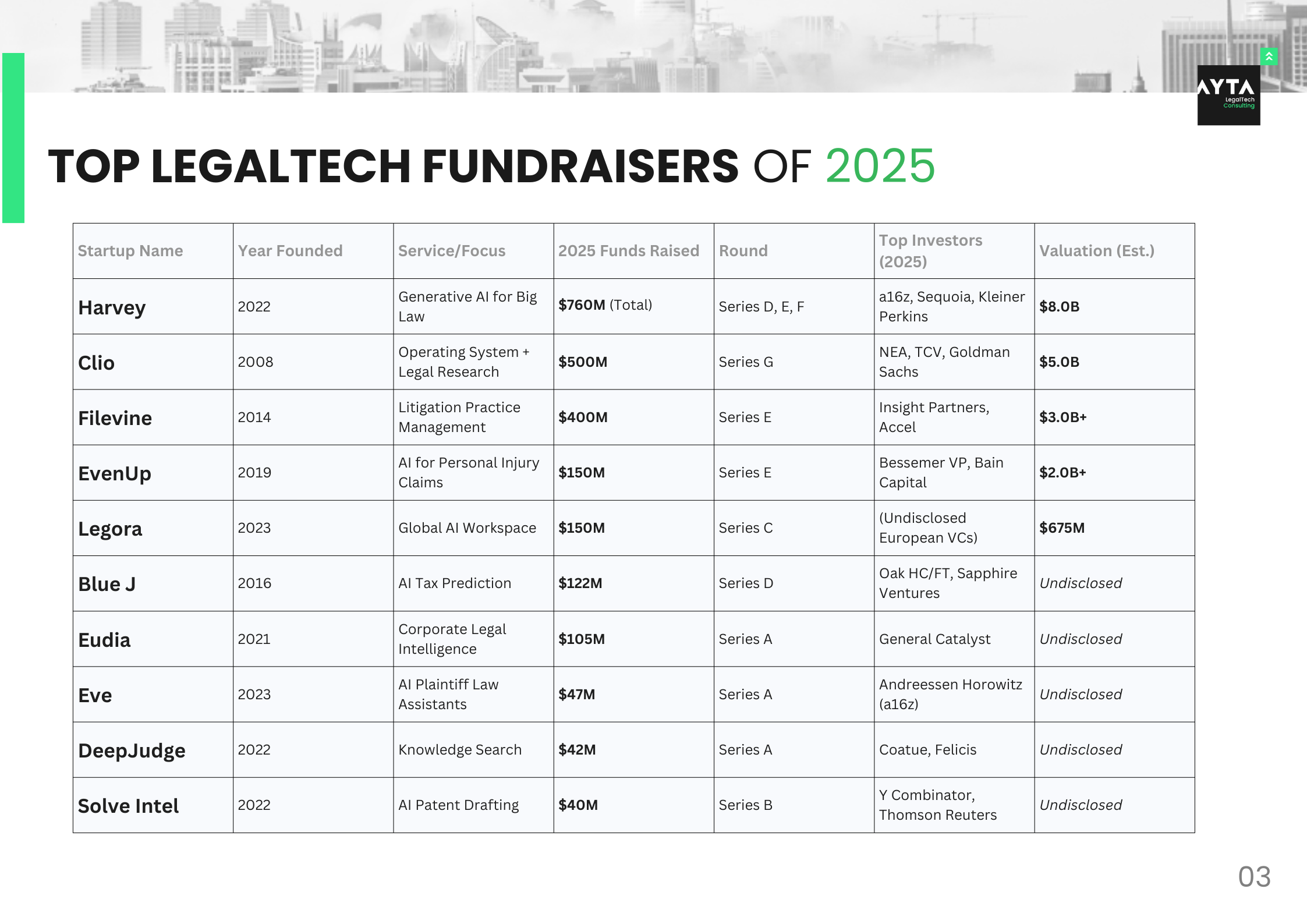

The 2025 fundraising leaderboard

A handful of companies effectively defined the 2025 fundraising narrative in legal tech.

Top funded LegalTech platforms in 2025

Across these companies, a consistent pattern emerges:

Deep workflow ownership (case management, claims processing, contract review, tax analysis) rather than generic AI features.

Strong network and data effects, often via embedded usage across thousands of firms and matters.

Investor syndicates that blend traditional growth equity with strategic or ecosystem players such as Thomson Reuters and GV.

Who actually wrote the big checks?

Capital in 2025 bifurcated into two clear groups: late-stage “kingmakers” and specialized funds building the next generation from Seed to Series B.

Late-stage kingmakers

These generalist and mega-funds dominated the largest rounds and effectively picked the global category leaders.

Andreessen Horowitz (a16z): Among the most aggressive, backing Harvey and Eve and positioning itself as a central architect of the legal AI stack.

NEA: Led Clio’s $500 million Series G, betting heavily on practice management plus research as the core operating system for the legal mid-market.

Insight Partners: Doubled down on “SaaS plus AI” with Filevine, reinforcing the view that legal infrastructure is a software-plus-intelligence story, not a tools story.

Bessemer Venture Partners: Played strongly in vertical AI, including EvenUp and Legora, aligning with its broader thesis on category-defining SaaS plus AI companies.

Sequoia and Kleiner Perkins: Anchored Harvey’s rise, signaling that the very top tier of Sand Hill Road sees vertical legal AI as a core frontier rather than a niche offshoot.

Specialized and strategic funds

Below the mega rounds, the groundwork for the 2027–2030 leaders is being laid by specialized and strategic capital.

The LegalTech Fund: Continued to specialize in Seed/Series A legaltech, reportedly closing a $100M+ second fund focused on AI-native legal workflows.

Oak HC/FT and Sapphire: Used their fintech and B2B SaaS expertise to back Blue J and other data-intensive, regulated-domain platforms.

Thomson Reuters Ventures: Pursued strategic stakes in companies like Solve Intel and others, aligning external innovation with its internal AI and content roadmap.

GV (Google Ventures): Participated in multiple Harvey rounds, aligning cloud and AI infrastructure bets with vertical legal adoption.

For founders, the implication is clear: late-stage capital now expects category ownership and scale economics, while early-stage capital is hunting for agentic, workflow-native products that can become the next Harvey, Clio, or Filevine rather than niche plug-ins.

New entrants and the agent-first wave

Despite capital concentration at the top, 2025 was not just a story of giants; it also produced a new cohort of “agent-first” startups that treat AI as the default actor, not an add-on.

Notable examples include:

ComplyJet: An AI-native security and compliance platform built specifically for fast-growing tech companies subject to complex regulatory obligations.

GitLaw: A “GitHub for lawyers” concept, offering version-controlled drafting for complex transactional work and making deal documents behave more like code.

Vulcan: A high-speed legal service delivery platform designed around AI-driven task routing and execution.

Struck: AI-assisted code and regulatory compliance tooling aimed at technology lawyers navigating fast-changing regulatory landscapes.

Mirror Mode by EvenUp: A flagship 2025 product that allows firms to clone a star partner’s writing style, widely cited as a key driver behind EvenUp’s valuation and fundraising momentum.

The common denominator: these companies assume the future legal stack is AI-orchestrated from day one, and design the user experience around delegation to agents, not manual configuration.

What the $4.3B year tells us

By year-end, legal tech had raised an estimated $4.3 billion in 2025—roughly 150% growth versus 2024—across around 155 funded startups and about 85 notable new entrants. The average age of Series A and above companies has settled around 4–5 years, which is typical of a market moving from discovery to scale.

For the global legaltech ecosystem, a few structural takeaways matter:

The stack is consolidating around a small group of global platforms that combine workflow, content, and AI.

Specialized vertical AI (tax, personal injury, patent drafting, corporate legal) is now a proven path to scale if the product deeply matches domain workflows.

Mid-tier point solutions without a clear wedge, network effect, or data moat will increasingly face either forced consolidation or capital starvation.

2026: what comes next

Looking ahead, the 2025 data points to three strong narratives for 2026 and beyond.

1. The death of the point solution

Cases like Robin AI’s distressed sale underscore how unforgiving the market has become toward standalone single-feature tools that don’t own a critical workflow or data layer. Expect 2026 to bring:

A wave of acqui-hires and roll-ups, as platforms buy capabilities rather than competing feature-by-feature.

Increasing pressure on incumbents to unify fragmented product lines into coherent platforms that support agentic workflows end to end.

2. The first major legaltech IPOs

With Clio at around a $5 billion valuation and Harvey approaching $8 billion, the sector now has companies with the scale, revenue profiles, and global customer bases to credibly test public markets. If macro conditions allow, 2026–2027 could see:

The first pure-play legaltech IPOs in North America or Europe.

A reset in how public markets value “legal AI” versus traditional legal software, with metrics shifting from seat-based licensing to usage- and outcome-based economics.

3. Sovereign legal AI and regional champions

There is growing demand, especially in Europe and Asia, for “sovereign legal AI”—tools that are compliant with local privacy regimes (GDPR and beyond), trained on local jurisprudence, and hosted in-region. Companies like Legora, and emerging players in markets such as Germany, France, the Nordics, Japan, and India, are well-positioned to:

Build regional AI workspaces that meet data-residency and sovereignty requirements.

Serve cross-border work where firms must navigate conflicting regulatory regimes without exposing sensitive data to US-centric infrastructures.

For global legaltech operators and investors, the 2025 fundraising cycle is less a spike and more a new baseline: legal is finally being treated as a mission-critical, data-rich industry where AI-native platforms can justify multi-billion-dollar bets. The next phase will reward those who can combine deep domain credibility with agentic AI, platform thinking, and a clear stance on sovereignty, security, and real-world adoption

.png)